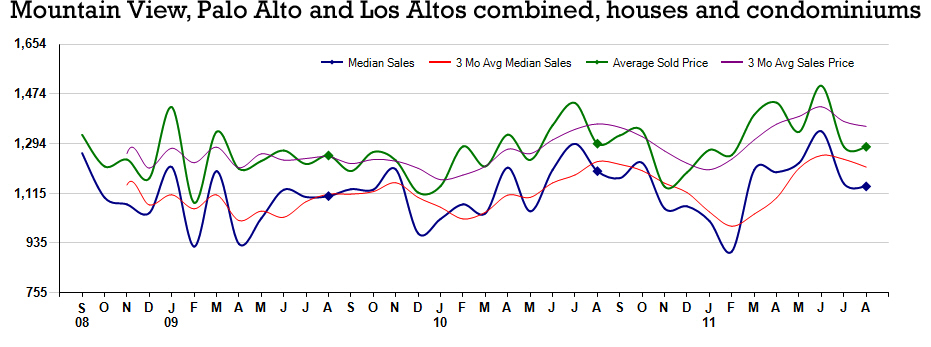

How does it look all combined??

This is the way the market looks for these 3 Cities combined, houses and condominiums and townhouses, all together, over the past 2 and a half years.

Some will describe it as “definitely hesitant”,

Some will say it is “getting better”,

Others will say that the worse was in mid 09.

It is difficult to interpret such graphs because a low average price per square foot can just mean that more properties of a larger size sold that month, and the median and average price mean something different, - although the curves are fairly parallel. This is a summary of many individual stories.

But one thing is certain, the market is alive and kicking here, and in most of the Silicon Valley.

Also, let’s remember that about 35% of houses sell for over asking price in the County, and a good 30 to 35% of sales are cash sales, with no loan involved … We are fortunate.

Curious about your City, or your zip code? Let me know, I can help ;-)

Francis

useful links

Remember: our Free E-Waste Collection and Shredding Event,

on: 10/22/11, Sat. 9 am to 4 pm for E-Waste Collection

10 am to 2 pm for Shredding.

address: 161 S. San Antonio Rd, Los Altos, CA 94022