Foreclosure Evictions Temporarily Suspended

Both Freddie Mac and Fannie Mae are temporarily suspending all scheduled evictions involving foreclosed occupied single-family 1- to 4- unit residences with owned mortgages beginning December 19, 2011 through January 2, 2012.

The suspension will apply only to eviction lockouts related to Freddie Ma and Fannie Mae owned REO properties and will not affect other pre- or post-foreclosure processes. During this period, legal and administrative proceedings for evictions may continue, but families living in foreclosed properties will be permitted to remain in the home.

Francis

useful links

Mortgage rates

Sunday, December 25, 2011

Friday, December 16, 2011

Silicon Valley Counties: real estate activity

To keep in perspective: a lot is being said in the press about real estate in the Bay Area, including a lot of foreclosures and short sales happening all the time. But really, when you add all properties combined, (houses and condominiums, townhouses, PUD’s etc…), what really happened to the market in our area in the past 3 years? I think simple graphs can help us understand how we fare here in the Silicon Valley. In the Counties of San Mateo & Santa Clara, let us look at a simple measure: the average sales price:

Individual Cities can be very different. For instance Palo Alto has the following history in the same 3 years, showing here in blue the average time to sell a home:

the variations in sales prices are not as steep as the averages in the County.

Let me know and I will prepare a study of your own City/ neighborhood.

Thanks for reading !

Francis

useful links

Mortgage rates

Individual Cities can be very different. For instance Palo Alto has the following history in the same 3 years, showing here in blue the average time to sell a home:

the variations in sales prices are not as steep as the averages in the County.

Let me know and I will prepare a study of your own City/ neighborhood.

Thanks for reading !

Francis

useful links

Mortgage rates

Friday, December 9, 2011

On the local political front, a little note on Sunnyvale...

The Silicon Valley Association of Realtors (SILVAR) Opposes Sunnyvale Plan to Regulate Real Estate Transactions

As part of the development of Sunnyvale's Climate Action Plan, the city is considering prohibiting the sale of property until an energy and water efficiency inspection is completed for owner occupied homes and energy efficiency retrofits are made to commercial property. The proposals were discussed as part of a city council study session this week.

SILVAR opposes this proposal because of the detrimental impact it will have on property owners and the ability to close transactions in Sunnyvale. Also, because the mandates would only impact properties at the time of sale, it would take decades before it would impact a significant amount of the housing stock.

SILVAR presented written testimony in opposition to the proposed mandate to the council, and SILVAR Past President Mark Burns had previously spoken at a meeting and asked the council to remove the recommendation from the draft report.

None of the council members spoke in favor of keeping the time of sale mandate in the draft. Council Member Chris Moylan made a strong statement in opposition to the recommendation. The draft climate action plan will be out for public comment and review over the next several months, so stay tuned for updates.

Thanks for reading.

Francis

useful links

Mortgage rates

As part of the development of Sunnyvale's Climate Action Plan, the city is considering prohibiting the sale of property until an energy and water efficiency inspection is completed for owner occupied homes and energy efficiency retrofits are made to commercial property. The proposals were discussed as part of a city council study session this week.

SILVAR opposes this proposal because of the detrimental impact it will have on property owners and the ability to close transactions in Sunnyvale. Also, because the mandates would only impact properties at the time of sale, it would take decades before it would impact a significant amount of the housing stock.

SILVAR presented written testimony in opposition to the proposed mandate to the council, and SILVAR Past President Mark Burns had previously spoken at a meeting and asked the council to remove the recommendation from the draft report.

None of the council members spoke in favor of keeping the time of sale mandate in the draft. Council Member Chris Moylan made a strong statement in opposition to the recommendation. The draft climate action plan will be out for public comment and review over the next several months, so stay tuned for updates.

Thanks for reading.

Francis

useful links

Mortgage rates

Friday, December 2, 2011

The Marriage of Weddings and Real Estate...

Many couples about to tie the knot are doing a different type of wedding registry nowadays, one that allows them to collect cash for a down payment on a home, according to a recent article in The Washington Times.

Dana Ostomel, founder of Deposit a Gift in New York City, says that about 15 % of their registries are to raise down-payment funds for a home and another 15 % are for home-improvement funds to pay for upgrades like a new roof or furniture. "Given that 75 % of today’s engaged couples already live together and are older, very often they are already established with the household basics that you find on a traditional registry," Ostomel said. "What they want is the gift of big-ticket items and longer term goals, like the gift of home ownership.”

Dana Ostomel, founder of Deposit a Gift in New York City, says that about 15 % of their registries are to raise down-payment funds for a home and another 15 % are for home-improvement funds to pay for upgrades like a new roof or furniture. "Given that 75 % of today’s engaged couples already live together and are older, very often they are already established with the household basics that you find on a traditional registry," Ostomel said. "What they want is the gift of big-ticket items and longer term goals, like the gift of home ownership.”

The FHA permits gifts from a wedding to be used as a down payment, but lenders are required to document that the funds are gifts. About 27 % of first-time home buyers use gift money from relatives and friends for a down payment, according to a 2010 National Association of REALTORS® Profile of Home Buyers and Sellers survey. Source: The Washington Times

Francis Rolland

useful links

Mortgage rates

The FHA permits gifts from a wedding to be used as a down payment, but lenders are required to document that the funds are gifts. About 27 % of first-time home buyers use gift money from relatives and friends for a down payment, according to a 2010 National Association of REALTORS® Profile of Home Buyers and Sellers survey. Source: The Washington Times

Francis Rolland

useful links

Mortgage rates

Tuesday, November 29, 2011

1st 10 Months, 2010 and 2011...

Curious to see the evolution of average prices, from one year to the next?

It turns out it is pretty similar.

Here looking at the compared graphs of both the County of San Mateo, and Santa Clara, from one year to the next:

The one thing that appears at this point is a slight decrease in prices of single family residences in the County of Santa Clara. But this happened too at the end of 2010. Overall the curves are fairly similar.

What is also apparent in these graphs is that the average values are higher in the County of San Mateo than in the County of Santa Clara.

Finally, the end of the year is looking up for the San Mateo County so far.

Francis

useful links

Mortgage rates

It turns out it is pretty similar.

Here looking at the compared graphs of both the County of San Mateo, and Santa Clara, from one year to the next:

The one thing that appears at this point is a slight decrease in prices of single family residences in the County of Santa Clara. But this happened too at the end of 2010. Overall the curves are fairly similar.

What is also apparent in these graphs is that the average values are higher in the County of San Mateo than in the County of Santa Clara.

Finally, the end of the year is looking up for the San Mateo County so far.

Francis

useful links

Mortgage rates

Tuesday, November 22, 2011

Real Estate Eye Candy...

The digital edition of the Previews Magazine winter issue has just been released. Click to see some of the most spectacular homes Northern California has to offer.

The digital edition of the Previews Magazine winter issue has just been released. Click to see some of the most spectacular homes Northern California has to offer.Francis Rolland

Mortgage rates

Thursday, November 17, 2011

Bay Area Investors...

Investors: the trend continues in the Bay Area with a lot of buyers investors:

- 17% in the County of Santa Clara,

- 21% in San Mateo County - 27.5% in Solano County

- 21% in San Mateo County - 27.5% in Solano County

- 25% Contra Costa County.

Over 20% of all purchases are all cash, with no loan involved.

In fact, an interesting phenomenon occurs in some depressed areas:

in some condominium complexes, where over 15% of the units are delinquent, (typical) banks will not lend… So this leaves only cash buyers as potential buyers of these properties. Obviously these buyers purchase the units for the long term, hoping that the real estate market will improve enough that the complex will go up in value. The rents have increased so much in the past 2 years that the return on investment makes it a very viable deal.

An other problem can occur there though: if more than 50% of the units in a complex are non owner-occupied, loan are also almost impossible to obtain - or more expensive. One of the rules of most lenders is that this important percentage has to be over 50%. So that would leave future buyers and future homeowners in those complexes with a difficult situation: potential buyers who need a loan may not want to pay the extra fees and rates in order to get these loans.

Do not underestimate the need for good advice when you purchase a condominium. A seasoned agent is a must, to make sure you are informed. Here is a good informational page on this "condominium"subject.

Thanks for reading.

Francis

useful links

Mortgage rates

- 17% in the County of Santa Clara,

- 25% Contra Costa County.

Over 20% of all purchases are all cash, with no loan involved.

In fact, an interesting phenomenon occurs in some depressed areas:

in some condominium complexes, where over 15% of the units are delinquent, (typical) banks will not lend… So this leaves only cash buyers as potential buyers of these properties. Obviously these buyers purchase the units for the long term, hoping that the real estate market will improve enough that the complex will go up in value. The rents have increased so much in the past 2 years that the return on investment makes it a very viable deal.

An other problem can occur there though: if more than 50% of the units in a complex are non owner-occupied, loan are also almost impossible to obtain - or more expensive. One of the rules of most lenders is that this important percentage has to be over 50%. So that would leave future buyers and future homeowners in those complexes with a difficult situation: potential buyers who need a loan may not want to pay the extra fees and rates in order to get these loans.

Do not underestimate the need for good advice when you purchase a condominium. A seasoned agent is a must, to make sure you are informed. Here is a good informational page on this "condominium"subject.

Thanks for reading.

Francis

useful links

Mortgage rates

Wednesday, November 9, 2011

Silicon Valley: housing inventory

To keep things in perspective, it is good to keep an eye on the inventory of homes for sale at a given point in time. Here is the inventory of all properties for sale (houses + PUD/condos) both in the whole County of Santa Clara, and in the area limited to the five Cities: Los Altos, Los Altos Hills, Palo Alto, Mountain View, and Menlo Park:

Lower inventory = tendency for prices to be sustained, or rise.

There are signifcantly fewer properties for sale now than last year. It is also interesting to note that the luxury market (over $1 million) has fewer homes on the market, which is reflecting the fact that the market has been more active in the past months.

Here in the Bay Area, as noted many times, demand is showing pretty strong fairly consistently.

As agents, we note that open houses are very busy, especially for houses, and certainly all the time for houses in the good school districts. In Palo Alto, multiple offers are the rule, as with all properties priced at market value, in good school districts.

As agents, we note that open houses are very busy, especially for houses, and certainly all the time for houses in the good school districts. In Palo Alto, multiple offers are the rule, as with all properties priced at market value, in good school districts.

It is worth noting again that about 30% of houses sell for over asking price in the County of Santa Clara.

A lot of them are foreclosures. - A foreclosure sale does not always mean that it is a fabulous deal, moneywise.

Interested in the same figures for only condominiums for instance? Let me know.

Francis Rolland

useful links

Mortgage rates

Lower inventory = tendency for prices to be sustained, or rise.

There are signifcantly fewer properties for sale now than last year. It is also interesting to note that the luxury market (over $1 million) has fewer homes on the market, which is reflecting the fact that the market has been more active in the past months.

Here in the Bay Area, as noted many times, demand is showing pretty strong fairly consistently.

It is worth noting again that about 30% of houses sell for over asking price in the County of Santa Clara.

A lot of them are foreclosures. - A foreclosure sale does not always mean that it is a fabulous deal, moneywise.

Interested in the same figures for only condominiums for instance? Let me know.

Francis Rolland

useful links

Mortgage rates

Friday, November 4, 2011

Buy now with 3.5% down payment...

If you have a stable income and if you are paying too much for rent, it can definitely make sense to buy with an FHA loan.

Many people believe that to even think of becoming a homeowner you must secure a 20% down payment. This is difficult to do for a lot of aspiring-to-be-homeowners. But there is another way:

think: " FHA loans ".

think: " FHA loans ".

- 3.5% down. Low down payment - less money out of pocket and 96.5% loan-to-value.

(Source: Freddie Mac)

Many people believe that to even think of becoming a homeowner you must secure a 20% down payment. This is difficult to do for a lot of aspiring-to-be-homeowners. But there is another way:

think: " FHA loans ".FHA facts to keep in mind:

- 100% Gift allowed for down payment and closing costs,

- Any buyer can buy like this, not just first-time home buyers,

- minimum FICO 640,

- Long term financing: 30 year fixed, or adjustable,

- Loan limits up to $625,500, depending on the County,

- Non occupant co-borrowers are ok

- Purchase and "refis" are allowed,Prior bankruptcies?: yes very possibly. See the specific rules, but on-time payments allow FHA borrowing fairly quickly afterwards.

|

There are some very nice homes that one can buy for less than $500,000 in Santa Clara for instance, and you'd only need ... about $20k. With an FHA loan you do pay what is called mortgage insurance, a way for the lender to be insured against potential future defaults. But even with this mortgage insurance, these loans can be pretty attractive when everything is said and done, because banks do not mind doing such loans: they have ... mortgage insurance. Hence the very attractive rates.

If this gives you food for thoughts, let me know: I can help! ...or for someone you know, pass it along!..

Francis

PS: Mortgage rates: Week ending 11/3/2011

- 30-yr. fixed: 4.0 fees/points: 0.7%

- 15-yr. fixed: 3.31 fees/points: 0.7%

- 1-yr. adjustable: 2.88% Fees/points: 0.6% (Source: Freddie Mac)

Friday, October 28, 2011

Who does not cringe at rejection?..

Triggers for rejection. - Loan rejection that is.

• Insufficient income: well, this is straightforward… But also, lenders typically look for at least a two-year track record of income, which could hurt those who have changed jobs recently.

• Insufficient income: well, this is straightforward… But also, lenders typically look for at least a two-year track record of income, which could hurt those who have changed jobs recently.

• Poor credit: Lenders typically reject applicants with FICO scores below 620.

• Low appraisal: One of the predominant reasons buyers are turned down for home loans is because the appraisal on the property is too low. If this is the case, the bank will often loan less, which can create a problem for the cash-tight buyers.

• Property problems: Sometimes issues turn up within a house, like a major repair or safety issue that needs to be addressed, before an application can be approved.

• Information mix-ups: Approximately 12 percent of new mortgage applications were denied because of unverifiable information or incomplete credit applications, according to the Federal Financial Institutions Examination Council.

The full story can be accessed here.

If you need any lender referrals, don't hesitate to contact me. When you buy a home or refinance, you rely a lot on your loan agent.

Thanks for reading!...

Francis

frolland.com

PS: Mortgage rates: Week ending 10/27/2011

- 30-yr. fixed: 4.11 fees/points: 0.8%

- 15-yr. fixed: 3.38 fees/points: 0.8%-

- 1-yr. adjustable: 2.94% Fees/points: 0.6%

(Source: Freddie Mac)

Last year, more than two million people were turned down for homes, according to federal data, often because the applicants didn’t meet certain lender requirements or because their applications were incomplete or otherwise problematic. With lenders’ underwriting criteria becoming more rigorous in recent years, it’s important buyers know the most common triggers for mortgage-loan rejection.

• Insufficient income: well, this is straightforward… But also, lenders typically look for at least a two-year track record of income, which could hurt those who have changed jobs recently.

• Cloudy financial picture: Generally, total debt payments, including the mortgage, cannot exceed 45 to 50 percent of a borrower’s adjusted gross monthly income. Overtime and bonuses are included only if the borrower has worked for the same employer at least two years, and has a history of receiving them.

• Poor credit: Lenders typically reject applicants with FICO scores below 620.

• Low appraisal: One of the predominant reasons buyers are turned down for home loans is because the appraisal on the property is too low. If this is the case, the bank will often loan less, which can create a problem for the cash-tight buyers.

• Property problems: Sometimes issues turn up within a house, like a major repair or safety issue that needs to be addressed, before an application can be approved.

• Information mix-ups: Approximately 12 percent of new mortgage applications were denied because of unverifiable information or incomplete credit applications, according to the Federal Financial Institutions Examination Council.

The full story can be accessed here.

If you need any lender referrals, don't hesitate to contact me. When you buy a home or refinance, you rely a lot on your loan agent.

Thanks for reading!...

Francis

frolland.com

PS: Mortgage rates: Week ending 10/27/2011

- 30-yr. fixed: 4.11 fees/points: 0.8%

- 15-yr. fixed: 3.38 fees/points: 0.8%-

- 1-yr. adjustable: 2.94% Fees/points: 0.6%

(Source: Freddie Mac)

Tuesday, October 25, 2011

Refinancing & the Economy .. A Missing Link ...

There is a lot of noise right now about the “occupy wall street” movement. And the economy is giving ulcers to everyone. The world is full of catch 22’s in many important areas. Consider the following situation if you have a second with me, and tell me if this is not illogical:

Someone wants to refinance their property but the value has gone down so much that it is under the value of the loan. The rules of the banks, the way they are right now, are such that the bank will not allow the borrower to refinance the same amount of loan as before (because of the “loan-to-value ratios” rules). How does that make sense? The lender is taking a much bigger risk in most cases by leaving someone obligated to pay a high interest rate that will sink them, when they could pay a lower rate and have a better chance of affording their loan.

The borrower, in front of such an illogical catch 22, decides to stop paying and to go to foreclosure. If you look at my previous blog, it is clear to many analysts that a lot of these borrowers are not inherently a “bad risk”, just because they decided to default on a loan that they cannot change. When these borrowers have only one default on their record, and it is this kind of default, they are often ready to buy something else, at today’s value, with today’s interest rate. It is often cheaper than to rent. But they cannot do it because of their credit history (since they just defaulted on a loan).

The system is blocked. It is thought that many people, if they were allowed to buy a new property, would prefer that option to renting.

- 1/ the market would be a lot less depressed, as many properties would sell instead of sitting forever,

- 2/ because more properties would sell, the market values would be more sustained and in many cases would slightly go up. This in turn would help the banks, since the total market value of their distressed properties would be higher.

This blog does not go into judging anyone, or deciding if it would be fair to do this or that. But the difficulty to refinance falls under rules that are counter-intuitive in my opinion.

As I write this I learn that the HARP program (see one of my previous blogs on refinancing) has just been expanded to the end of 2013, and removed the 125% ceiling on “loan-to-value” cap for fixed rate mortgages backed by Fannie Mae and Freddie Mac. More on this PDF from the Federal Housing Finance Agency. However, I need to underline that it is for mortgages backed by FNMA and Freddie Mac only...

Still, it is estimated that between 1.5 and 2 million people may take advantage of these new rules. (just heard on NPR).

Couldn't all the banks think in the same manner, for their own ultimate good? And couldn't they waive some qualifying rules on a case-by-case basis? - It would make a lot of "cents" to them in the end.

Couldn't all the banks think in the same manner, for their own ultimate good? And couldn't they waive some qualifying rules on a case-by-case basis? - It would make a lot of "cents" to them in the end.

Thanks for reading,

Francis

Friday, October 21, 2011

The luxury market in the Silicon Valley….

A total of 207 homes sold for more than $1 million in Santa Clara County in August, essentially flat from the previous month’s 208 transactions but down from the 221 sales recorded in August 2010.

However, the median sale price of a million-dollar home in the South Bay climbed to $1,387,000, up 2.7 percent from the $1.35 million median sale price recorded in July and August of last year.

Other metrics also showed the high-end market continues to recover: There were 41 multi-million-dollar sales last month, up from 34 in July and 36 in August 2010. And sellers received 100 percent of their asking price on average, up from 98 percent a year ago and 99 percent the previous month.

The figures were derived from Multiple Listing Service data of all homes sold in Santa Clara County for more than $1 million in August.

“The luxury segment of the Silicon Valley housing market continues to strengthen, along with the high-end markets in other parts of the Bay Area,” said Rick Turley, president of Coldwell Banker Residential Brokerage. “Both sales and prices are firming up in the South Bay, San Francisco, the Peninsula and Marin County. That could be a leading indicator of how the overall market will fare in the months ahead.”

Turley noted that the high-end market often recovers first following a downturn. Last month, DataQuick, the La Jolla-based real estate research firm, reported that overall sales in the Bay Area last month rose 12.2 percent, although the median price dipped 3.9 percent.

Some key findings from this month’s Coldwell Banker Residential Brokerage luxury report:

• The most expensive sale in Santa Clara County last month was a five-bedroom, nine-bath 6,400-square foot home in Los Gatos that sold for $5.2 million;

• Los Altos boasted the most million-dollar sales last month with 43, followed by Palo Alto with 33, San Jose with 32, Saratoga with 29, and Cupertino with 17;

• Homes closing last month stayed on the market an average of 38 days, the same as the previous month and up from 36 days a year ago.

The Silicon Valley Luxury Housing Market Report is a monthly report by Coldwell Banker Residential Brokerage, a specialist in high-end real estate sales.

Thanks for reading!

Francis Rolland

useful links

However, the median sale price of a million-dollar home in the South Bay climbed to $1,387,000, up 2.7 percent from the $1.35 million median sale price recorded in July and August of last year.

Other metrics also showed the high-end market continues to recover: There were 41 multi-million-dollar sales last month, up from 34 in July and 36 in August 2010. And sellers received 100 percent of their asking price on average, up from 98 percent a year ago and 99 percent the previous month.

The figures were derived from Multiple Listing Service data of all homes sold in Santa Clara County for more than $1 million in August.

“The luxury segment of the Silicon Valley housing market continues to strengthen, along with the high-end markets in other parts of the Bay Area,” said Rick Turley, president of Coldwell Banker Residential Brokerage. “Both sales and prices are firming up in the South Bay, San Francisco, the Peninsula and Marin County. That could be a leading indicator of how the overall market will fare in the months ahead.”

Turley noted that the high-end market often recovers first following a downturn. Last month, DataQuick, the La Jolla-based real estate research firm, reported that overall sales in the Bay Area last month rose 12.2 percent, although the median price dipped 3.9 percent.

Some key findings from this month’s Coldwell Banker Residential Brokerage luxury report:

• The most expensive sale in Santa Clara County last month was a five-bedroom, nine-bath 6,400-square foot home in Los Gatos that sold for $5.2 million;

• Los Altos boasted the most million-dollar sales last month with 43, followed by Palo Alto with 33, San Jose with 32, Saratoga with 29, and Cupertino with 17;

• Homes closing last month stayed on the market an average of 38 days, the same as the previous month and up from 36 days a year ago.

The Silicon Valley Luxury Housing Market Report is a monthly report by Coldwell Banker Residential Brokerage, a specialist in high-end real estate sales.

Thanks for reading!

Francis Rolland

useful links

Wednesday, October 19, 2011

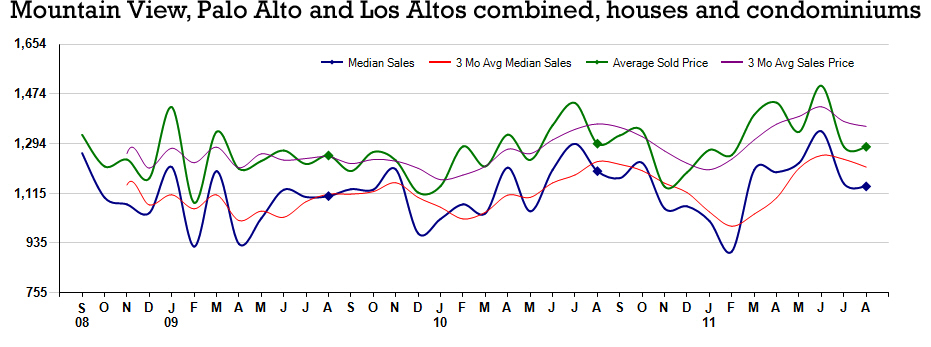

Palo Alto, Mountain View, Los Altos …

We know that the market is very localized, and that even within a City the market is markedly different from low-end to high-end, from an area to an other, and of course whether it is a house or a condominium.

How does it look all combined??

This is the way the market looks for these 3 Cities combined, houses and condominiums and townhouses, all together, over the past 2 and a half years.

Some will describe it as “definitely hesitant”,

Some will say it is “getting better”,

Others will say that the worse was in mid 09.

It is difficult to interpret such graphs because a low average price per square foot can just mean that more properties of a larger size sold that month, and the median and average price mean something different, - although the curves are fairly parallel. This is a summary of many individual stories.

But one thing is certain, the market is alive and kicking here, and in most of the Silicon Valley.

Also, let’s remember that about 35% of houses sell for over asking price in the County, and a good 30 to 35% of sales are cash sales, with no loan involved … We are fortunate.

Curious about your City, or your zip code? Let me know, I can help ;-)

Francis

useful links

Remember: our Free E-Waste Collection and Shredding Event,

on: 10/22/11, Sat. 9 am to 4 pm for E-Waste Collection

10 am to 2 pm for Shredding.

address: 161 S. San Antonio Rd, Los Altos, CA 94022

How does it look all combined??

This is the way the market looks for these 3 Cities combined, houses and condominiums and townhouses, all together, over the past 2 and a half years.

Some will describe it as “definitely hesitant”,

Some will say it is “getting better”,

Others will say that the worse was in mid 09.

It is difficult to interpret such graphs because a low average price per square foot can just mean that more properties of a larger size sold that month, and the median and average price mean something different, - although the curves are fairly parallel. This is a summary of many individual stories.

But one thing is certain, the market is alive and kicking here, and in most of the Silicon Valley.

Also, let’s remember that about 35% of houses sell for over asking price in the County, and a good 30 to 35% of sales are cash sales, with no loan involved … We are fortunate.

Curious about your City, or your zip code? Let me know, I can help ;-)

Francis

useful links

Remember: our Free E-Waste Collection and Shredding Event,

on: 10/22/11, Sat. 9 am to 4 pm for E-Waste Collection

10 am to 2 pm for Shredding.

address: 161 S. San Antonio Rd, Los Altos, CA 94022

Friday, October 14, 2011

KnowYourOptions.com ...

Homeowners in difficulty: KnowYourOptions.com

For homeowners who are in difficulty to make their mortgage payments or cannot refinance, there are several options other than Short Sales or letting the property be sold through the foreclosure process.

Fannie Mae has set up a website: www.knowyouroptions.com/ . That site lists the five possible options that sellers should explore with their legal and financial advisors before deciding to list their property as a Short Sale or letting it go through a foreclosure action, if the loan is owned by Fannie Mae.

Fannie Mae has set up a website: www.knowyouroptions.com/ . That site lists the five possible options that sellers should explore with their legal and financial advisors before deciding to list their property as a Short Sale or letting it go through a foreclosure action, if the loan is owned by Fannie Mae.

This web site is all about getting informed, knowing all the possibilities available to be able to stay in your home, the options if you do have to leave your home, and how to contact a help center – if the loan is owned by Fannie Mae.

In-person and telephone support for homeowners is available in the “Mortgage Help Centers”.

These Centers have been established to help homeowners with loans owned by Fannie Mae. At a Mortgage Help Center, one can meet directly with dedicated on-site staff and experienced housing advisors to discuss one’s mortgage situation. English and Spanish advisors are available, and all services offered by the Fannie Mae Mortgage Help Center are FREE.

Of course, hopefully this is not something that is needed...

Francis Rolland

useful links

PS: Mortgage rates: Week ending 10/06/2011:

- 30-yr. fixed: 3.94 fees/points: 0.8%

- 15-yr. fixed: 3.26 fees/points: 0.8%

- 1-yr. adjustable: 2.95% Fees/points: 0.5%

(Source: Freddie Mac)

Worth noting: our Free E-Waste Collection and Shredding Event,

on: 10/22/11, Sat. 9 am to 4 pm for E-Waste Collection

10 am to 2 pm for Shredding.

address: 161 S. San Antonio Rd, Los Altos, CA 94022

For homeowners who are in difficulty to make their mortgage payments or cannot refinance, there are several options other than Short Sales or letting the property be sold through the foreclosure process.

This web site is all about getting informed, knowing all the possibilities available to be able to stay in your home, the options if you do have to leave your home, and how to contact a help center – if the loan is owned by Fannie Mae.

In-person and telephone support for homeowners is available in the “Mortgage Help Centers”.

These Centers have been established to help homeowners with loans owned by Fannie Mae. At a Mortgage Help Center, one can meet directly with dedicated on-site staff and experienced housing advisors to discuss one’s mortgage situation. English and Spanish advisors are available, and all services offered by the Fannie Mae Mortgage Help Center are FREE.

Of course, hopefully this is not something that is needed...

Francis Rolland

useful links

PS: Mortgage rates: Week ending 10/06/2011:

- 30-yr. fixed: 3.94 fees/points: 0.8%

- 15-yr. fixed: 3.26 fees/points: 0.8%

- 1-yr. adjustable: 2.95% Fees/points: 0.5%

(Source: Freddie Mac)

Worth noting: our Free E-Waste Collection and Shredding Event,

on: 10/22/11, Sat. 9 am to 4 pm for E-Waste Collection

10 am to 2 pm for Shredding.

address: 161 S. San Antonio Rd, Los Altos, CA 94022

Friday, September 30, 2011

Refinancing? Current loan limits expire this week...

Current loan limits expire this week (today on Friday).

Current conforming loan limits are scheduled to expire Friday, Sept. 30. The maximum FHA, Fannie Mae, and Freddie Mac conforming loan limit will decline to $625,500 beginning Oct. 1, 2011, from the current $729,750 limit, though the majority of counties will fall far below the $625,500 maximum.

Current conforming loan limits are scheduled to expire Friday, Sept. 30. The maximum FHA, Fannie Mae, and Freddie Mac conforming loan limit will decline to $625,500 beginning Oct. 1, 2011, from the current $729,750 limit, though the majority of counties will fall far below the $625,500 maximum.

The conforming loan limit determines the maximum size of a mortgage that FHA, Fannie Mae, and Freddie Mac government-sponsored enterprises (GSEs) can buy or guarantee. Non-conforming or jumbo loans typically carry a higher mortgage interest rate than a conforming loan and require a higher down payment, increasing the monthly payment and negatively impacting housing affordability for California home buyers.

An estimated 30,000 people will be impacted in California by this new limit.

If you are thinking of refinancing, or a purchase, I can certainly help you choose a reliable, professional lender.

Francis Rolland

Silicon Valley real estate

Local real estate links.

►worthy to note: our next E-Waste collection and shredding event: 10/22/11

at: 161 S. San Antonio Rd, Los Altos, CA 94022.

It's easy, it's free, it's green! Stop by for free shredding service and bring your electronic recyclables with you! TV's, cell phones, batteries, computer stuff.... ;-)

The conforming loan limit determines the maximum size of a mortgage that FHA, Fannie Mae, and Freddie Mac government-sponsored enterprises (GSEs) can buy or guarantee. Non-conforming or jumbo loans typically carry a higher mortgage interest rate than a conforming loan and require a higher down payment, increasing the monthly payment and negatively impacting housing affordability for California home buyers.

An estimated 30,000 people will be impacted in California by this new limit.

If you are thinking of refinancing, or a purchase, I can certainly help you choose a reliable, professional lender.

Francis Rolland

Silicon Valley real estate

Local real estate links.

►worthy to note: our next E-Waste collection and shredding event: 10/22/11

at: 161 S. San Antonio Rd, Los Altos, CA 94022.

It's easy, it's free, it's green! Stop by for free shredding service and bring your electronic recyclables with you! TV's, cell phones, batteries, computer stuff.... ;-)

Friday, September 23, 2011

Can you be an "accidental landlord" ?

Reading this article from Rismedia called: “sign of the times, accidental landlords”, it reminded me of several situations I have seen recently here in the Bay Area, with clients who became exactly that: an accidental landlord.

What do you do indeed when you need to move, but your property would not sell for what you bought it for?

One solution is to sell it at a loss, and recuperate this loss in the new purchase, which is going to be less expensive too; but you cannot do this as easily nowadays. It used to be that you could purchase a home and get a “bridge loan” from the house you were moving from. The bridge loan was predicated on the house being sold within 2 or 3 months. Banks did not have any problem doing this because they were pretty sure your old house would sell fairly quickly. You cannot get such a bridge loan today, and therefore you have to sell your previous house first, and then move to temporary housing and start looking for your new house. Not very convenient…

Another solution is to buy subject to the sale of your current home. This is harder to do than to say; often it means you’d have to pay more, to compensate for a weak bargaining position. It is almost impossible to do if you are looking for a desirable property, and other people want it too.

The remaining option is to rent out your previous house and purchase your new home. But there again the banks are a lot tighter with their money (hum.., your money…), and the rules are much stricter. The ideal is when you have enough income to qualify for 2 loans easily. If you are not in this ideal case, you need to show that your previous house has a tenant in place before they will lend you on your purchase. And there you go, you are an “accidental landlord”.

People do not intend to remain a landlord for long, just the time for the market to improve enough that it will make sense to sell. But actually, if you are going to have savings, it makes sense to spread them over several investment vehicles: the usual suspects are “real estate”, CD’s, bonds, stocks and cash. Over the long term, a real estate investment can be a good retirement account. But remember to check with your tax advisor: depending on your specific situation, the tax implications will not be the same.

If you think you may find yourself in such a situation, call me to discuss your options.

Thanks for reading!

Francis

http://www.frolland.com/

http://www.francisrolland.com/

Friday, September 16, 2011

Fix Ups for Property Resale

Are you a homeowner preparing your home for sale? If you are, you may want to consider these 6 real estate fix up tips. They will help you increase your chances of getting the most return at the time of sale, for a modest cost. We can often overlook the simplest things but these 6 tips will ensure that you optimize for the maximum payout.

"Money wisely spent is money wisely earned."

"Money wisely spent is money wisely earned."- Cleaning and de-cluttering - costs $290 but yields a $1,990 Return (put things in boxes, since they will end up in boxes anyway)

- Brightening - costs $375 but yields a $1,550 Return (clean and clear windows, update light fixtures)...

- Smart staging - costs $550 but yields a $2,194 Return

- Landscaping enhancements - costs $540 but yields a $1,932 return (new flowers, nice colors, clean up...)

- Repairing electrical or plumbing - costs $535 but yields a $1,505 Return - time to repair these little things that have been left alone...

- Replacing or shampooing dirty carpets - costs $647 but yields a $1,739 Return

The yields are estimates of course, but a good indication of the results.

The ROI (return on investment) on performing these property fix ups is pretty good, so consider them closely. The time spent performing the tasks are plainly worth the effort.

The 6 home fix up tips were the result of a Home Sale Maximizer Survey released by HomeGain.com. - the result of a survey of nearly 600 real estate professionals to try to find out what pays the most. The survey was to aid home sellers in determining what to consider to prepare their homes for sale time.

Let me know, as always, how I can help!

Francis,

Thursday, September 8, 2011

Buyer beware! lenders need to know everything!

Buyers beware... When applying for a loan: lenders need to know everything!

1- All funds used for the down payment and closing costs are going to be very carefully scrutinized by the lender:

1- All funds used for the down payment and closing costs are going to be very carefully scrutinized by the lender:

4- Things not to do during an escrow:

useful links

1- All funds used for the down payment and closing costs are going to be very carefully scrutinized by the lender:- you must provide detailed and accurate information to show which accounts the funds are in and where the funds are coming from,

- you must document the source of any funds that have been in your accounts for less than 2 months,

- any changes that occur to your financial condition will need to be explained to the lender,

- changes to your assets, employment, income or credit scores during the escrow could jeopardize your ability to qualify,

- provide complete documents, - all pages!

- provide documents with names, addresses and account numbers.

2- The lender is going to require a letter of explanation and/or support documentation for:

- recent inquiries or derogatory items on your credit report,

- recent deposits, transfers of money etc... in your accounts,

- evidence earnest money deposit has cleared your account. ... hum, they don't trust much...

3- If you are receiving Gift Funds the lender will require:

a gift letter signed by you and the gift donor,

a gift letter signed by you and the gift donor,- evidence of the donors ability to gift the funds (bank statement),

- evidence of the receipt of the gift funds, in your account.

- do not transfer funds between accounts, nor make large deposits into your bank accounts,

- do not buy a car!... or spend large amounts of money on stuff..

- do not change jobs,

- do not close or open credit card accounts.

Yes, it is a real experience, to get a loan nowadays! ;-)

For lenders referrals, do not hesitate to contact me.

FrancisFriday, August 19, 2011

Why it is a good time to buy real estate...

Real estate is positioned well for the future...

From our Coldwell Banker blog...

* "Baby boomers are in their prime real estate buying years and are 78 million strong.

* The Pew Research Center reports minority homeownership levels still have room for improvement. The gaps between white and minority households remain significant with homeownership rates for Asians (59.1 percent), African-Americans (47.5 percent) and Latinos (48.9 percent) well below the 74.9 percent among whites.

* Immigrants are moving to the U.S. by the tune of 1.1-1.5 million a year depending on the source. These are legal immigrants who add value to our country and society. They need housing.

* Echo boomers will likely have similar economic impact in coming years that their baby boomers parents have had through their lives. Echo boomers are born between 1977 and 1994 and are 73 million strong and according to the Joint Center for Housing Studies at Harvard University, 4 million turn 21 each year.

* Household formation is also an important statistic. The Joint Center for Housing Studies at Harvard University projects at least 1.25 million households will be created annually from 2010-2020 and will be led by the echo boomers.

* Household formation is also an important statistic. The Joint Center for Housing Studies at Harvard University projects at least 1.25 million households will be created annually from 2010-2020 and will be led by the echo boomers.

* Between 2010 and 2020, the Census Bureau projects U.S. household growth to be in the range of 1.25 to 1.5 million per year, which will create an additional demand for housing. This should equate to a demand for 12.5 -15 million total new households during this decade.

* People move for lifestyle. There have been 4 million marriages and a record more than 8 million babies born in the last two years indicating there is demand for housing. Many of these growing families have not bought a home and are either renting or living with family as they save for a down payment. We know there is pent up demand." ....

* People move for lifestyle. There have been 4 million marriages and a record more than 8 million babies born in the last two years indicating there is demand for housing. Many of these growing families have not bought a home and are either renting or living with family as they save for a down payment. We know there is pent up demand." ....

Why is now a smart time to buy?

"I.I.I.P. Inventory, interest rates, incentives and price. In most markets around the nation, home inventory has increased giving buyers a greater choice. At the same time, mortgage rates remain at near historic lows and home prices have seemingly stabilized. 2010 saw median prices increase slightly by 0.2% to $172,900. This has made home affordability the best since at least 1973 and maybe ever."

Thanks for reading, and let me know how I can help, always!

Francis

Silicon Valley Real Estate

Los Altos Specialist

Rates:

Mortgage rates: Week ending 8/4/2011 30-yr. fixed: 4.39 fees/points: 0.8% 15-yr. fixed: 3.54 fees/points: 0.7% 1-yr. adjustable: 3.02% Fees/points: 0.5% (Source: Freddie Mac)

From our Coldwell Banker blog...

* "Baby boomers are in their prime real estate buying years and are 78 million strong.

* The Pew Research Center reports minority homeownership levels still have room for improvement. The gaps between white and minority households remain significant with homeownership rates for Asians (59.1 percent), African-Americans (47.5 percent) and Latinos (48.9 percent) well below the 74.9 percent among whites.

* Immigrants are moving to the U.S. by the tune of 1.1-1.5 million a year depending on the source. These are legal immigrants who add value to our country and society. They need housing.

* Echo boomers will likely have similar economic impact in coming years that their baby boomers parents have had through their lives. Echo boomers are born between 1977 and 1994 and are 73 million strong and according to the Joint Center for Housing Studies at Harvard University, 4 million turn 21 each year.

* Between 2010 and 2020, the Census Bureau projects U.S. household growth to be in the range of 1.25 to 1.5 million per year, which will create an additional demand for housing. This should equate to a demand for 12.5 -15 million total new households during this decade.

Why is now a smart time to buy?

"I.I.I.P. Inventory, interest rates, incentives and price. In most markets around the nation, home inventory has increased giving buyers a greater choice. At the same time, mortgage rates remain at near historic lows and home prices have seemingly stabilized. 2010 saw median prices increase slightly by 0.2% to $172,900. This has made home affordability the best since at least 1973 and maybe ever."

Thanks for reading, and let me know how I can help, always!

Francis

Silicon Valley Real Estate

Los Altos Specialist

Rates:

Mortgage rates: Week ending 8/4/2011 30-yr. fixed: 4.39 fees/points: 0.8% 15-yr. fixed: 3.54 fees/points: 0.7% 1-yr. adjustable: 3.02% Fees/points: 0.5% (Source: Freddie Mac)

Wednesday, July 20, 2011

Valuable Appliance Longevity Report Every Home Owner Must Have

Have you ever thought about the life expectancy of your household appliances? How about the materials used to build your home? Well, if you are like many home owners today, you probably haven't given it much thought at all. I mean, who really needs to know how long the shingles on the roof are going to last, anyway, right? But, that is just the point; there are some things, you, the home owner, need to know.

Whether you are buying a home or thinking of selling your home, it is important to understand the estimated life expectancy of all your appliances and other home materials. Buying or selling a house without factoring in the cost to fix aging materials can cost you in the long run.

Whether you are buying a home or thinking of selling your home, it is important to understand the estimated life expectancy of all your appliances and other home materials. Buying or selling a house without factoring in the cost to fix aging materials can cost you in the long run.

There are many factors involved that can age a household appliance like a refrigerator or building material such as siding.

• Weather

• Maintenance

• How an item is used.

Here are some examples depending on above factors:

• A refrigerator may last up to 13 years.

• Cooks, - your kitchen cabinets have a life expectancy of 50 years.

• Outdoor lovers, your outside deck has only a life span of 20 years.

• Vinyl Siding will last for the lifetime of the house, and

• Your wood floor will endure for 100 years. Of course, all under ideal circumstances.

The NAHB, National Association of Home Builders released a report in 2007 entitled, "Study of Life Expectancy of Home Components." They list appliances, building materials, as well as other components you may never have thought about. The comprehensive report is only 19 pages long yet boasts as a worthy read of any home owner or potential buyer.

The NAHB, National Association of Home Builders released a report in 2007 entitled, "Study of Life Expectancy of Home Components." They list appliances, building materials, as well as other components you may never have thought about. The comprehensive report is only 19 pages long yet boasts as a worthy read of any home owner or potential buyer.

Let me know, as always, how I can help!

Francis

Silicon Valley Specialist

Local Real Estate resources

Silicon Valley Market Trends

There are many factors involved that can age a household appliance like a refrigerator or building material such as siding.

• Weather

• Maintenance

• How an item is used.

Here are some examples depending on above factors:

• A refrigerator may last up to 13 years.

• Cooks, - your kitchen cabinets have a life expectancy of 50 years.

• Outdoor lovers, your outside deck has only a life span of 20 years.

• Vinyl Siding will last for the lifetime of the house, and

• Your wood floor will endure for 100 years. Of course, all under ideal circumstances.

Let me know, as always, how I can help!

Francis

Silicon Valley Specialist

Local Real Estate resources

Silicon Valley Market Trends

Thursday, July 14, 2011

Do you rent out one of your properties?

Reporting is now easier for mom-and-pop landlords.

I had send earlier in the year an email to all my clients who rented out a property, to alert them about a new IRS reporting requirement.

![]()

Households that find renters for a second property but are not in the business of real estate don’t have to send an IRS Form 1099 to vendors if the vendors do more than $600 worth of work in a year. Landlords have faced the 1099 reporting requirement for a while, and that requirement continues to apply to them, but last year the requirement was extended to households and entities that rent out property as a sideline but are not in the rental housing trade.

Francis Rolland

Silicon Valley real estate

I had send earlier in the year an email to all my clients who rented out a property, to alert them about a new IRS reporting requirement.

Good news: this has changed, for the better. Here is how:

Households that find renters for a second property but are not in the business of real estate don’t have to send an IRS Form 1099 to vendors if the vendors do more than $600 worth of work in a year. Landlords have faced the 1099 reporting requirement for a while, and that requirement continues to apply to them, but last year the requirement was extended to households and entities that rent out property as a sideline but are not in the rental housing trade.

The National Association of Realtors and others strongly opposed that expansion and succeeded in persuading lawmakers to repeal it, which Congress did.

President Obama signed the repeal into law in late April, so, now the requirement applies as it always has: just to those in the business of real estate.

Francis Rolland

Tuesday, July 12, 2011

Study: Homeowners Who Default on Mortgage Alone Not a Credit Risk

Today, many homeowners who defaulted on their mortgage payments have asked the question, "Will my mortgage delinquencies make me a higher credit risk to lenders?"

![]() A homeowner needs to consider what establishes poor credit and good credit in the eyes of the lender. Surprisingly enough, if you have other debt that you are in good standing with, such as credit cards or an auto loan, you will be less likely deemed as a credit risk. Those who have defaulted on their mortgage payment as well as other accounts are higher risks to a lending institution. The study below reveals why.

A homeowner needs to consider what establishes poor credit and good credit in the eyes of the lender. Surprisingly enough, if you have other debt that you are in good standing with, such as credit cards or an auto loan, you will be less likely deemed as a credit risk. Those who have defaulted on their mortgage payment as well as other accounts are higher risks to a lending institution. The study below reveals why.

Transunion. , a global leader in credit and information management, released a study which stated, "...consumers who only defaulted on their mortgage during the economic recession were far better risks than those consumers who went delinquent on multiple credit accounts." This particular study explained that consumers, who were only default with their mortgage payment, displayed stronger ability to stay current with other loans.

"There appears to be a pocket of opportunity among mortgage-only defaulters that is not the result of excess liquidity, but rather the unique circumstances of the recent recession," said Steve Chaouki, group vice president in TransUnion's financial services business unit. "This new market segment that the recession created is an important one for lenders to understand. They have the potential, today, to be stronger and more reliable customers."

![]() Breaking it down…

Breaking it down…

• The lack of cash flow that resulted in defaulted mortgage payments does not by itself make the consumer “high risk” to a lender.

• You are a risk if you have multiple delinquencies on other accounts including the mortgage.

• You are not a risk if you have mortgage-only defaults but are current with other debt, such as a car loan or credit card.

In conclusion, if you are a mortgage-only defaulter you have more hope than those who are not and should not consider yourself a high risk. For more information, here is the link again to the Transunion study Mortgage-only Defaulters.

Let me know, as always, how I can help!

Francis

Silicon Valley Specialist

Local _Real Estate resources

Silicon Valley Market Trends

Good question.

On the surface, it is obvious that falling behind and becoming consistently delinquent on any bill is not a financially sound thing to do. However, your credit rating may not be as tarnished as some would leave you to believe. A homeowner needs to consider what establishes poor credit and good credit in the eyes of the lender. Surprisingly enough, if you have other debt that you are in good standing with, such as credit cards or an auto loan, you will be less likely deemed as a credit risk. Those who have defaulted on their mortgage payment as well as other accounts are higher risks to a lending institution. The study below reveals why.

A homeowner needs to consider what establishes poor credit and good credit in the eyes of the lender. Surprisingly enough, if you have other debt that you are in good standing with, such as credit cards or an auto loan, you will be less likely deemed as a credit risk. Those who have defaulted on their mortgage payment as well as other accounts are higher risks to a lending institution. The study below reveals why.Mortgage-Only Defaulters

Transunion. , a global leader in credit and information management, released a study which stated, "...consumers who only defaulted on their mortgage during the economic recession were far better risks than those consumers who went delinquent on multiple credit accounts." This particular study explained that consumers, who were only default with their mortgage payment, displayed stronger ability to stay current with other loans.

"There appears to be a pocket of opportunity among mortgage-only defaulters that is not the result of excess liquidity, but rather the unique circumstances of the recent recession," said Steve Chaouki, group vice president in TransUnion's financial services business unit. "This new market segment that the recession created is an important one for lenders to understand. They have the potential, today, to be stronger and more reliable customers."

• The lack of cash flow that resulted in defaulted mortgage payments does not by itself make the consumer “high risk” to a lender.

• You are a risk if you have multiple delinquencies on other accounts including the mortgage.

• You are not a risk if you have mortgage-only defaults but are current with other debt, such as a car loan or credit card.

In conclusion, if you are a mortgage-only defaulter you have more hope than those who are not and should not consider yourself a high risk. For more information, here is the link again to the Transunion study Mortgage-only Defaulters.

Let me know, as always, how I can help!

Francis

Silicon Valley Specialist

Local _Real Estate resources

Silicon Valley Market Trends

Thursday, July 7, 2011

Refinancing problems? here is a suggestion...

Are you trying to refinance but you cannot because your equity is too low?

Are you trying to refinance but you cannot because your equity is too low? This is the classic catch 22 in which you cannot take advantage of great rates because the bank’s appraisal is too low.

The HARP refinancing program is addressing precisely this need. HARP: Home Affordable Refinance Program, administered by Fannie Mae and Freddie Mac.

Good News !!

Some limitations apply of course, but fairly reasonable. One of them, for instance, is that you need to spend more than 31% of your pre-tax income on your mortgage payment. (thank you Nicolas! ;-) for the input). Check out the details on the Freddie Mac web site, or the Fannie Mae web site: Fannie Mae web site.

Another program worthy of noting if you have financial problems: the "Making Home Affordable" Program.

Thanks for reading!

Francis

Silicon Valley real estate

Search the MLS

Saturday, July 2, 2011

Some perspective on the Silicon Valley market....

Some recent headlines turned heads and generated a lot of questions among my clients recently, headlines such as: “Case-Schiller Down 5.1%; What Will Stop It?” and “The Depressing State of Housing”.

What is really going on in the Valley? I find that chosen graphs speak much better than headlines. Comparison of the first 5 months of last year, with the same months this year, for the Counties of Santa Clara and San Mateo:

![]()

This graph shows roughly the same movement as last year. If anything, it shows a better situation, since we do not have in 2011 the government incentives for 1st time homebuyers that we had in 2010 (Calif. 1st time homebuyers credits, and federal incentives). These created last year a rush to buy before June, which does not exist in 2011.

Comparison charts for Sunnyvale and Mountain View:

![]()

Comparison charts for Los Altos and Palo Alto:

![]()

Average prices can vary a lot from month to month. These charts just show that overall the market is fairly the same as last year, at the very least.

Thanks for reading!

Francis

Mortgage rates: Week ending 6/23/2011: - 30-yr. fixed: 4.50 fees/points: 0.8% - 15-yr. fixed: 3.69 fees/points: 0.7% - 1-yr. adjustable: 2.99% Fees/points: 0.5% (Source: Freddie Mac)

Silicon Valley real estate resource

Real estate links of interest

What is really going on in the Valley? I find that chosen graphs speak much better than headlines. Comparison of the first 5 months of last year, with the same months this year, for the Counties of Santa Clara and San Mateo:

This graph shows roughly the same movement as last year. If anything, it shows a better situation, since we do not have in 2011 the government incentives for 1st time homebuyers that we had in 2010 (Calif. 1st time homebuyers credits, and federal incentives). These created last year a rush to buy before June, which does not exist in 2011.

Comparison charts for Sunnyvale and Mountain View:

Thanks for reading!

Francis

Mortgage rates: Week ending 6/23/2011: - 30-yr. fixed: 4.50 fees/points: 0.8% - 15-yr. fixed: 3.69 fees/points: 0.7% - 1-yr. adjustable: 2.99% Fees/points: 0.5% (Source: Freddie Mac)

Silicon Valley real estate resource

Real estate links of interest

Subscribe to:

Posts (Atom)