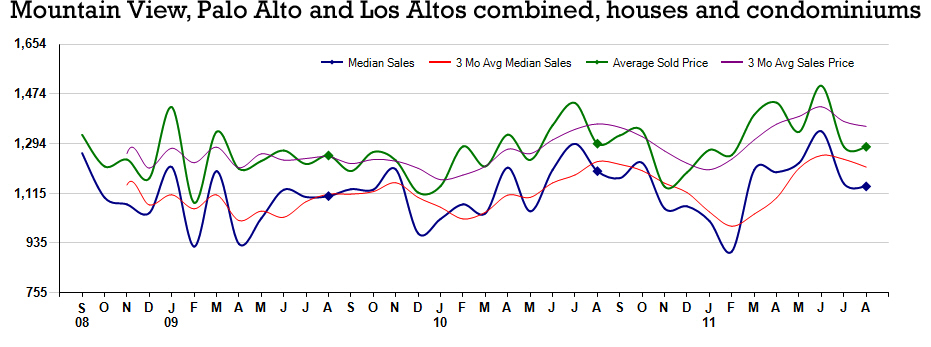

There is a lot of noise right now about the “occupy wall street” movement. And the economy is giving ulcers to everyone. The world is full of catch 22’s in many important areas. Consider the following situation if you have a second with me, and tell me if this is not illogical:

Someone wants to refinance their property but the value has gone down so much that it is under the value of the loan. The rules of the banks, the way they are right now, are such that the bank will not allow the borrower to refinance the same amount of loan as before (because of the “loan-to-value ratios” rules). How does that make sense? The lender is taking a much bigger risk in most cases by leaving someone obligated to pay a high interest rate that will sink them, when they could pay a lower rate and have a better chance of affording their loan.

The borrower, in front of such an illogical catch 22, decides to stop paying and to go to foreclosure. If you look at my previous blog, it is clear to many analysts that a lot of these borrowers are not inherently a “bad risk”, just because they decided to default on a loan that they cannot change. When these borrowers have only one default on their record, and it is this kind of default, they are often ready to buy something else, at today’s value, with today’s interest rate. It is often cheaper than to rent. But they cannot do it because of their credit history (since they just defaulted on a loan).

The system is blocked. It is thought that many people, if they were allowed to buy a new property, would prefer that option to renting.

- 1/ the market would be a lot less depressed, as many properties would sell instead of sitting forever,

- 2/ because more properties would sell, the market values would be more sustained and in many cases would slightly go up. This in turn would help the banks, since the total market value of their distressed properties would be higher.

This blog does not go into judging anyone, or deciding if it would be fair to do this or that. But the difficulty to refinance falls under rules that are counter-intuitive in my opinion.

As I write this I learn that the HARP program (see one of my previous blogs on refinancing) has just been expanded to the end of 2013, and removed the 125% ceiling on “loan-to-value” cap for fixed rate mortgages backed by Fannie Mae and Freddie Mac. More on this PDF from the Federal Housing Finance Agency. However, I need to underline that it is for mortgages backed by FNMA and Freddie Mac only...

Still, it is estimated that between 1.5 and 2 million people may take advantage of these new rules. (just heard on NPR).

Couldn't all the banks think in the same manner, for their own ultimate good? And couldn't they waive some qualifying rules on a case-by-case basis? - It would make a lot of "cents" to them in the end.

Couldn't all the banks think in the same manner, for their own ultimate good? And couldn't they waive some qualifying rules on a case-by-case basis? - It would make a lot of "cents" to them in the end.

Thanks for reading,

Francis